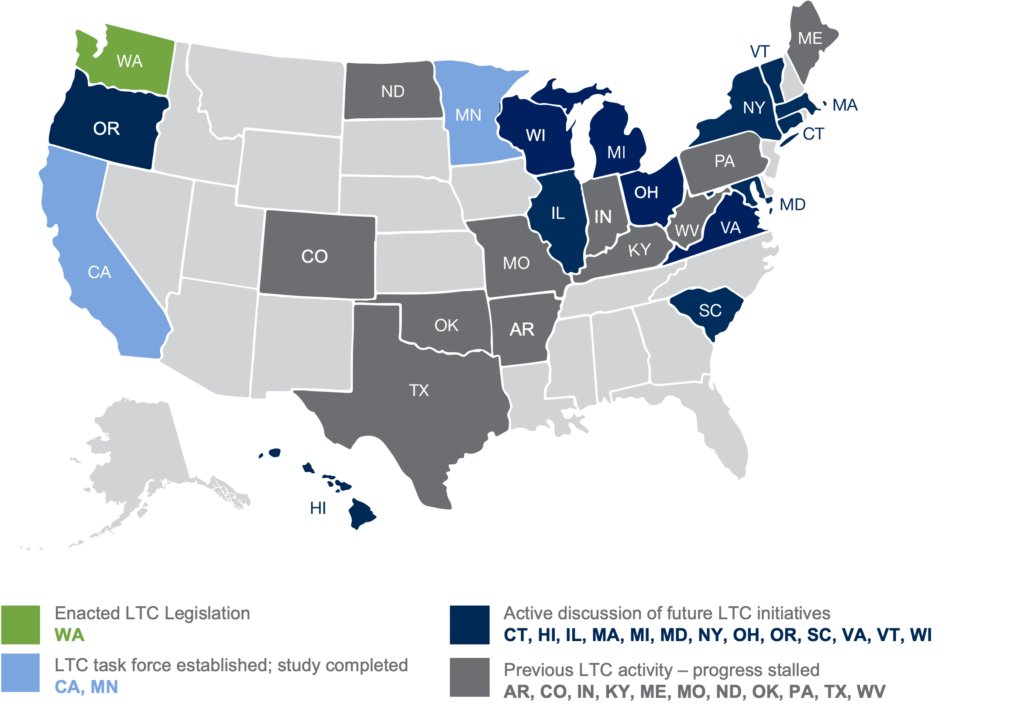

Did you know? Even though 72% of long term care is publicly funded,2 the vast majority of public funding requires very strict asset and income spend down to qualify. To address this significant budgetary burden, many states are considering implementing new programs which may include new payroll taxes, tax credits and incentives, or rate change regulation.

Outside of Washington State, should any of the programs currently being evaluated become law, securing this coverage may help you obtain an exemption from payroll taxes or obtaining tax credits or deductions based on whatever comes to fruition, if anything, in any state.